Why US financial institutions care about Solvency II regulations

In this article, read about the implications of Solvency II and Solvency UK on American financial institutions.

5 min read

Blog

CWAN empowers insurers to meet the evolving demands of Solvency II and Solvency UK regulatory frameworks, delivering daily‑reconciled data, automated workflows, and expert support on regulatory guidance.

Stay current without manual intervention with embedded regulatory updates.

Achieve governance, accuracy, and version control with a single, auditable data source.

Build complex portfolios, multi-jurisdiction accounting, and custom analytics.

Align with EIOPA and PRA regulatory changes all on one platform.

Eliminate spreadsheet‑based workflows with automated reporting that reduces time and risk.

Adhere to compliance requirements with regulatory onboarding, training, and expert support.

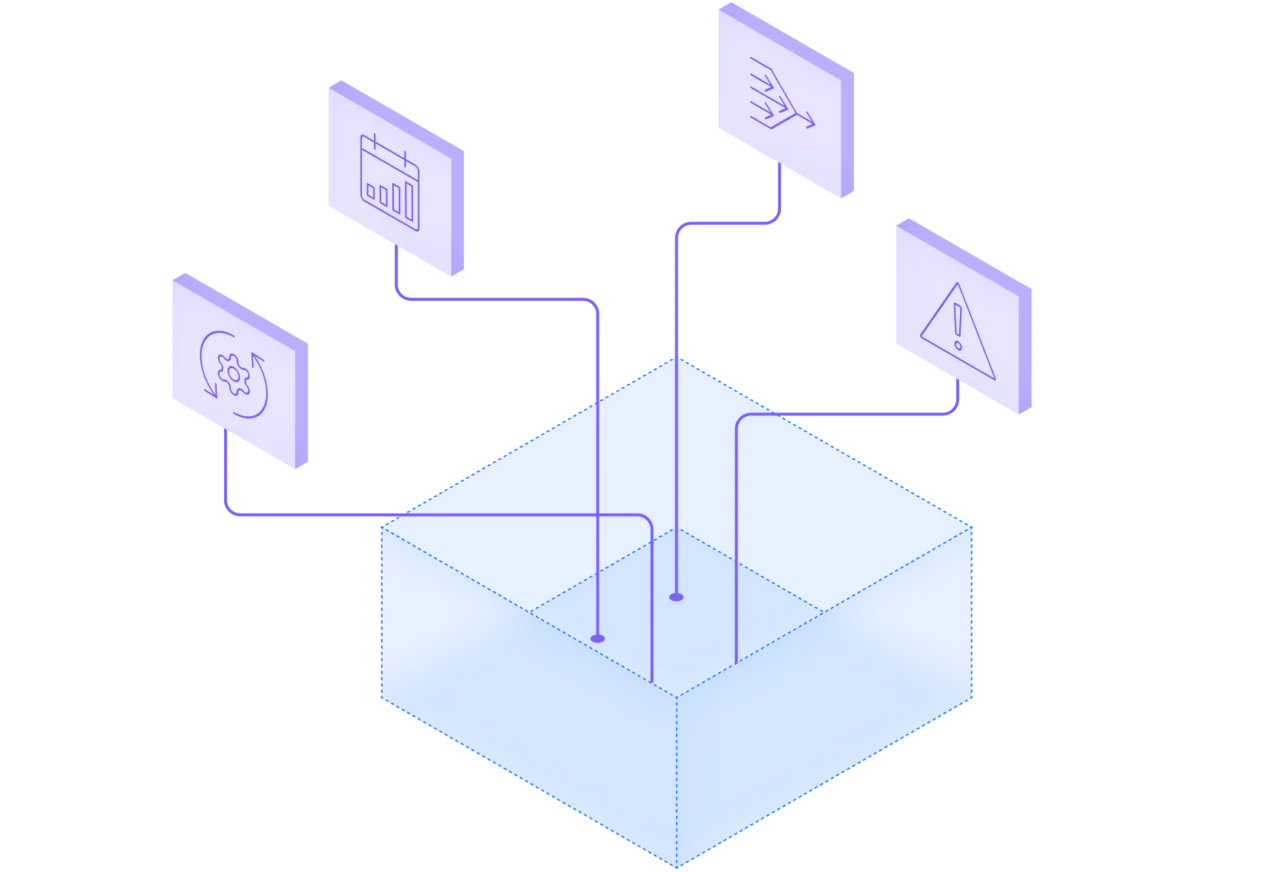

Cloud-based architecture gathers investment data across custodians, markets, and internal systems, reconciles it daily, and delivers a single trusted data source.

Pre-built, EIOPA- and PRA-compliant Pillar 3 QRT financial disclosure, including templates such as List of Assets (x.06.02), Fund Look-Through (x.06.03), and Open Derivatives (x.08.01).

Supplementary modules for Pillar 1 Regulatory Capital calculations ensure your reporting aligns with the latest EIOPA and PRA regulatory framework.

Simplify your regulatory reporting process with CWAN’s regulatory reporting to minimize compliance and operational risk.

Solvency II is a comprehensive regulatory framework for the insurance and reinsurance industry in the European Union, setting prudential requirements and risk management standards for the financial stability and soundness of insurance companies.

Solvency II compliance is mandatory for:

Compliance with Solvency II is crucial to ensure the financial stability, risk management, and regulatory adherence of entities operating in the EU insurance sector.

Solvency II is built on three pillars:

Solvency II: Solvency II is a European Union regulatory framework that applies to insurance and reinsurance companies operating within the EU. It sets out prudential requirements, risk management standards, and reporting and disclosure obligations for the entire EU insurance industry. It aims to create a harmonized and consistent regulatory environment across the EU member states.

Solvency UK: Solvency UK, often referred to as the UK’s implementation of Solvency II, is the application of Solvency II principles in the UK. It is how the UK transposed Solvency II requirements into its national legislation. While it closely aligns with Solvency II, there are some specific UK adaptations and regulations that reflect the unique features of the UK insurance market.

Solvency II requires insurers to adopt a more risk-aware approach, leading to a shift in business models, product portfolios, and investment strategies. Insurers must develop more risk-adequate products, align their investments with liabilities, and prioritize capital efficiency while maintaining regulatory compliance.

Solvency II regulatory authorities are increasingly focusing on climate and sustainability risks. There is a growing emphasis on integrating environmental, social, and governance (ESG) factors into risk assessments and reporting.

Technology is crucial for Solvency II compliance, enabling efficient data management, risk modelling, regulatory reporting, and automating compliance processes. Technology also uses advanced analytics to assess and manage risks more effectively.

Stay compliant and ahead of regulatory changes with CWAN’s platform and specialist support.

In this article, read about the implications of Solvency II and Solvency UK on American financial institutions.

This article will review some of the key takeaways from the PRA’s (Prudential Regulatory Authority) proposals for the Solvency UK changes.

The Solvency UK and Solvency II regulatory rulebooks are being updated this year with new rules which will further reduce operational efficiency for organizations not leveraging Clearwater.