Why US financial institutions care about Solvency II regulations

In this article, read about the implications of Solvency II and Solvency UK on American financial institutions.

5 min read

Blog

Bring capital calculations, regulatory validation, and QRT reporting together on a transparent, audit-ready foundation.

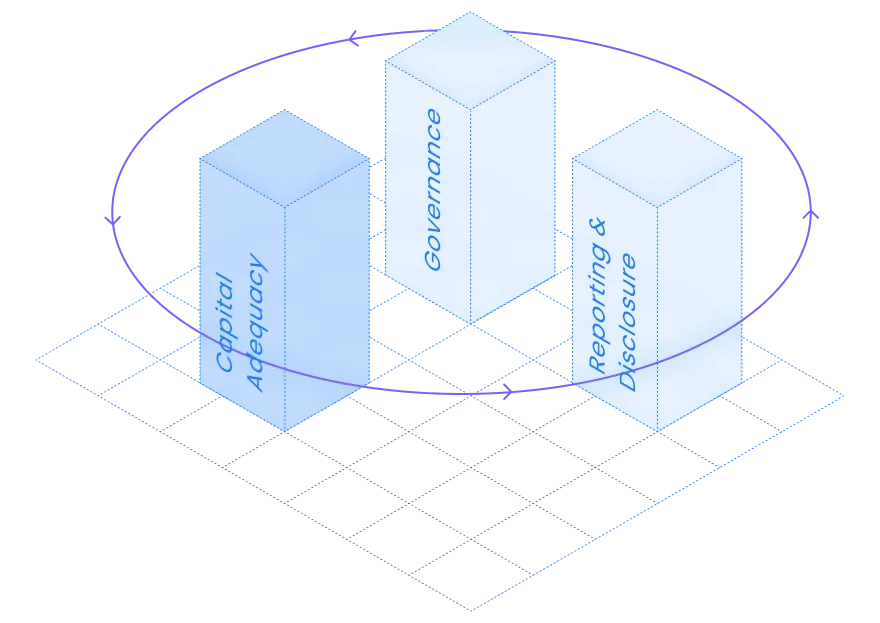

Pillar 1 defines capital requirements under the Solvency II framework, including the Solvency Capital Requirement (SCR) and Minimum Capital Requirement (MCR).

Clearwater supports Pillar 1 by:

By standardizing calculation logic and reducing spreadsheet dependency, Clearwater strengthens capital consistency and reduces operational modeling risk.

Pillar 2 focuses on governance, internal controls, and the Own Risk and Solvency Assessment (ORSA).

Clearwater supports Pillar 2 by strengthening the underlying control environment through:

While Clearwater does not replace governance frameworks or ORSA narrative processes, it provides the data integrity, transparency, and control evidence that support supervisory review and internal oversight.

Pillar 3 governs regulatory reporting through Quantitative Reporting Templates (QRTs) and disclosures. Clearwater supports Pillar 3 by:

This reduces manual intervention while improving reporting accuracy and audit defensibility.

Clearwater’s reporting framework strengthens capital transparency, improves consistency, and reduces operational exposure.

Allocate capital in a way that supports growth, returns, and strategic flexibility — without breaching regulatory constraints.

Minimize errors, spreadsheet dependency, and governance gaps that could lead to misstatement of regulatory capital.

Show regulators, auditors, and boards that capital calculations are accurate, traceable, and aligned to prescribed methodologies.

Request a working session to review scope, methodology coverage, and reporting controls.

In this article, read about the implications of Solvency II and Solvency UK on American financial institutions.

This article will review some of the key takeaways from the PRA’s (Prudential Regulatory Authority) proposals for the Solvency UK changes.

The Solvency UK and Solvency II regulatory rulebooks are being updated this year with new rules which will further reduce operational efficiency for organizations not leveraging Clearwater.

Solvency II requires insurers to calculate the Solvency Capital Requirement (SCR) using prescribed stress factors, maintain sufficient own funds to cover SCR and MCR thresholds, implement robust governance and risk management controls, and produce regulator-ready QRT outputs, including XBRL when required.

Clearwater supports investment-related Standard Formula SCR calculations and populates investment-related QRTs from reconciled data, with embedded validation controls and audit traceability to support supervisory review.

Solvency II applies to insurance and reinsurance undertakings authorized within the European Economic Area (EEA). It also applies at the group level to insurance groups headquartered in the EU and, in certain cases, to third-country groups with EU-regulated entities. Solvency UK applies to insurers regulated by the UK Prudential Regulation Authority (PRA).

Clearwater supports insurers operating under Solvency II and Solvency UK by centralizing investment data, applying Standard Formula investment risk calculations, and populating investment-related QRTs within a controlled, traceable workflow designed for supervisory scrutiny.

Non-compliance essentially means an insurer is not properly managing the relationship between its assets and liabilities, and poses severe financial, operational, and regulatory risks. Failure to comply with Solvency II requirements can result in:

By structuring capital calculation and reporting within a governed system, Clearwater helps insurers move from reactive remediation to defensible, repeatable compliance.

Solvency II: Solvency II is a European Union regulatory framework that applies to insurance and reinsurance companies operating within the EU. It sets out prudential requirements, risk management standards, and reporting and disclosure obligations for the entire EU insurance industry. It aims to create a harmonized and consistent regulatory environment across the EU member states.

Solvency UK: Solvency UK, often referred to as the UK’s implementation of Solvency II, is the application of Solvency II principles in the United Kingdom. It is how the UK transposed Solvency II requirements into its national legislation. While it closely aligns with Solvency II, there are some specific UK adaptations and regulations that reflect the unique features of the UK insurance market.

Yes. Clearwater supports Solvency UK reporting under the PRA framework.

Where Solvency UK diverges from EU Solvency II — such as calibration adjustments or reporting distinctions — Clearwater applies jurisdiction-specific logic to reflect applicable requirements. This allows insurers operating across EU and UK entities to manage reporting within a unified capital infrastructure.

Clearwater supports:

This enables insurers to manage capital calculations and supervisory reporting within a controlled, defensible framework.

Yes. Solvency II is an EU-wide regulatory framework. Clearwater supports Solvency II reporting requirements applicable across EU member states, including:

Jurisdiction-specific supervisory interpretations (e.g., local regulator guidance) are addressed as part of regulatory scoping and implementation.

Where firms operate under multiple capital regimes simultaneously, Clearwater enables consistent data integrity and control standards while applying the distinct methodologies required by each supervisory authority. Clearwater supports multi-jurisdiction reporting by:

Clearwater maintains reporting-period version control and preserves historical snapshots of calculation inputs, validation results, and QRT outputs. This allows insurers to reproduce prior submissions with full traceability for audit and supervisory review.